-

Jul 16, 2026

Jul 16, 2026 -

Comment: 0

Comment: 0

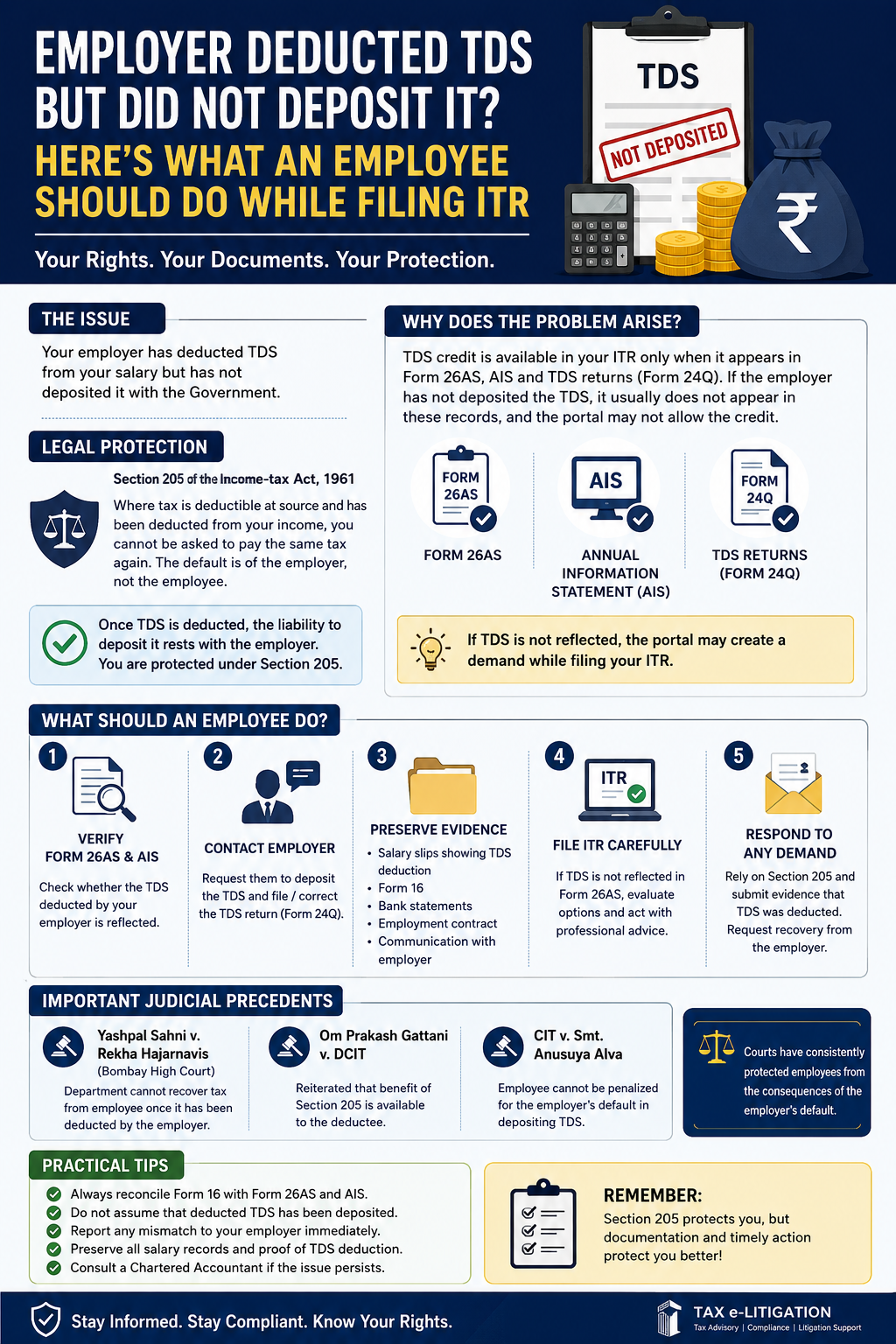

Employer Deducted TDS but Did Not Deposit It? Here's What an Employee Should Do While Filing the Income Tax Return

Every year, thousands of salaried taxpayers rely on their employers to deduct and deposit Tax Deducted at Source (TDS) with the Central Government. However, situations sometimes arise where an employer deducts TDS from an employee's salary but fails to deposit it with the Income-tax Department. This often creates confusion when the employee discovers that the TDS is not reflected in Form 26AS or the Annual Information Statement (AIS) while filing the Income Tax Return (ITR).

The important question is: Can the employee be denied TDS credit or asked to pay tax again?

The answer lies in the provisions of the Income-tax Act, 1961 and several judicial pronouncements.

Legal Protection under Section 205 of the Income-tax Act, 1961

Section 205 of the Income-tax Act provides a significant safeguard to taxpayers. It states that where tax is deductible at source and has been deducted from the income of the assessee, the assessee shall not be called upon to pay that tax again.

In simple terms, once an employer has deducted TDS from an employee's salary, the liability to deposit that tax rests entirely with the employer. The Income-tax Department cannot legally recover the same tax again from the employee merely because the employer failed to deposit it.

The employer becomes an "assessee in default" under the Act and is liable for interest, penalties, and other consequences prescribed by law.

Why Does the Problem Arise During ITR Filing?

Although the law protects the employee, the practical difficulty arises because the Income-tax portal grants TDS credit primarily based on information available in:

- Form 26AS

- Annual Information Statement (AIS)

- TDS returns filed by the employer (Form 24Q)

If the employer has not deposited the deducted TDS or has failed to file the TDS return correctly, the TDS amount generally does not appear in Form 26AS. Consequently, the portal may not automatically allow the employee to claim the credit, resulting in an unexpected tax demand while filing the return.

What Should an Employee Do?

1. Verify Form 26AS and AIS

Before filing the Income Tax Return, carefully verify whether the TDS deducted by the employer is reflected in Form 26AS and AIS. Any mismatch should be identified immediately.

2. Contact the Employer

Inform the employer about the discrepancy and request them to:

- Deposit the deducted TDS immediately.

- File or revise the TDS return (Form 24Q), if required.

- Issue a corrected Form 16.

Many cases are resolved once the employer updates the TDS records.

3. Preserve Documentary Evidence

Employees should maintain proper documentation to establish that TDS was actually deducted from their salary. These documents may include:

- Salary slips showing TDS deduction.

- Form 16 issued by the employer.

- Bank statements showing salary credited.

- Employment contract or appointment letter.

- Email correspondence or written communication with the employer regarding TDS.

These documents become extremely valuable if any dispute arises later.

4. File the Income Tax Return Carefully

If the employer has not deposited the TDS and the credit is unavailable on the portal, the employee should evaluate the available options based on the facts of the case.

In many situations, employees choose to follow up with the employer for correction before filing the return. Where this is not possible and a demand is generated, the employee should preserve all documentary evidence and be prepared to explain that TDS was deducted but not deposited.

Professional advice should be obtained before deciding the most appropriate course of action, particularly in cases involving substantial amounts.

5. Respond to Any Tax Demand

If the Income-tax Department raises a demand due to non-reflection of TDS, the employee should submit a detailed response relying upon Section 205 of the Income-tax Act along with documentary evidence proving that TDS was deducted from the salary.

The employee should request that recovery proceedings be initiated against the employer, who is legally responsible for depositing the deducted tax.

Important Judicial Precedents

Indian courts have consistently protected employees in such situations. Some of the important decisions include:

1. Yashpal Sahni v. Rekha Hajarnavis (Bombay High Court)

The Bombay High Court held that once tax has been deducted from the employee's salary, the department cannot recover the same amount again from the employee merely because the employer failed to deposit it.

2. Om Prakash Gattani v. DCIT

The court reaffirmed that the benefit of Section 205 is available to the deductee where tax has actually been deducted.

3. CIT v. Smt. Anusuya Alva

The court observed that the employee cannot be penalized for the employer's default in depositing TDS.

These judgments reinforce the principle that the burden of the employer's non-compliance cannot be shifted to an honest taxpayer.

Practical Advice for Salaried Taxpayers

Before filing your Income Tax Return:

- Always reconcile Form 16 with Form 26AS and AIS.

- Do not assume that TDS deducted from salary has been deposited.

- Immediately report any mismatch to your employer.

- Preserve all salary records and proof of TDS deduction.

- Consult a Chartered Accountant if the employer refuses to deposit the TDS or the Income-tax Department raises a demand.

Conclusion

The Income-tax Act clearly protects employees from double taxation where TDS has already been deducted from their salary. Section 205 ensures that the employee cannot be compelled to pay tax again merely because the employer failed to deposit the deducted amount.

However, from a practical standpoint, employees should remain vigilant by regularly checking Form 26AS, AIS, and Form 16 before filing their Income Tax Return. Early detection of discrepancies and timely follow-up with the employer can prevent unnecessary notices, litigation, and financial hardship.

Understanding your rights under the Income-tax Act and maintaining proper documentation are the best safeguards against the consequences of an employer's default.

Post a comment